Are Pakistani taxpayers and businesses prepared for the upcoming tax reforms? The Finance Minister has unveiled substantial updates to the nation’s tax framework through the Finance Act 2025.

This legislation seeks to reform a plethora of tax laws, revising critical statutes such as the Income Tax Ordinance 2001, Sales Tax Act 1990, and Customs Act 1969.

Grasping these changes is imperative for taxpayers to adeptly navigate the revamped tax terrain.

Key Takeaways

- Overview of the Finance Act 2025 and its objectives.

- Updates to key tax laws in Pakistan.

- Implications of the tax reforms for taxpayers.

- Key highlights of the Finance Act 2025.

- Importance of understanding the new tax legislation.

Understanding the Finance Act 2025: An Overview

The Finance Act 2025 heralds a transformative shift in Pakistan’s fiscal framework, designed to enhance revenue streams and stabilize the national economy. This legislative initiative stems from a meticulous analysis by the government, aimed at harmonizing tax regulations with contemporary economic realities.

Legislative Background and Passage

The passage of the Finance Act 2025 followed an exhaustive process of deliberation and amendment to extant tax legislation. This legislative evolution was necessitated by the imperative to update tax statutes, ensuring their efficacy in the prevailing economic milieu.

Key Objectives and Government Vision

The government’s vision for the Finance Act 2025 encompasses not only the augmentation of revenue but also the allure of foreign investment and the stimulation of economic expansion. The legislation’s primary objectives revolve around revenue generation through the introduction of novel tax brackets and the revision of prevailing tax rates, with a concurrent focus on stabilizing the economy by bolstering critical sectors.

Revenue Generation Goals

The Finance Act 2025 seeks to augment revenue through a suite of tax reforms. The government’s strategy involves the implementation of new tax brackets and the recalibration of existing tax rates to achieve this objective.

Economic Stabilization Measures

Economic stabilization is a cornerstone of the Finance Act 2025. The government’s strategy includes the provision of support to key sectors, coupled with the implementation of measures aimed at fostering economic growth and stability.

| Key Areas | Proposed Changes | Expected Outcomes |

|---|---|---|

| Revenue Generation | New tax slabs and revised tax rates | Increased government revenue |

| Economic Stabilization | Support for key sectors | Promoted economic growth and stability |

Legal Framework and Amendments

The Finance Act 2025 heralds a paradigm shift in Pakistan’s fiscal domain, introducing profound alterations to the tax regime. This legislation, aimed at simplifying tax compliance, curbing evasion, and augmenting revenue, marks a critical juncture in the nation’s economic trajectory.

Updates to the Income Tax Ordinance 2001

The Finance Act 2025 introduces seminal revisions to the Income Tax Ordinance 2001, with a focus on widening the tax net and incrementing tax rates for specific income segments. These modifications are intended to bolster revenue streams and foster tax equity, underpinning the government’s fiscal policy objectives.

Modifications to the Sales Tax Act 1990

Revisions to the Sales Tax Act 1990 encompass recalibrated tax rates and expanded tax brackets, with the objective of streamlining sales tax collection and diminishing exemptions. This necessitates a recalibration of business operations to ensure adherence to the revised regulatory framework.

Changes in the Customs Act 1969

The Finance Act 2025 further refines the Customs Act 1969, recalibrating import duties to safeguard domestic industries and enhance revenue generation. These adjustments will significantly influence importers and exporters, compelling them to navigate the updated customs regulations.

A tax expert opines, “The Finance Act 2025 represents a significant stride towards establishing a more equitable and efficacious tax system in Pakistan.” These amendments reflect the government’s dedication to elevating tax compliance and revenue generation, underscoring a critical phase in the nation’s economic development.

Why Pakistani Taxpayers Should Care About the Finance Act 2025

The imperative for Pakistani taxpayers to grasp the nuances of the Finance Act 2025 cannot be overstated. This legislation heralds a paradigm shift in taxation, with far-reaching implications for compliance and tax optimization.

Compliance Requirements and Deadlines

It is imperative for taxpayers to remain abreast of the enhanced compliance mandates and deadlines stipulated by the Finance Act 2025. The legislation imposes more stringent reporting and filing timelines, necessitating a heightened level of vigilance to avert any non-compliance.

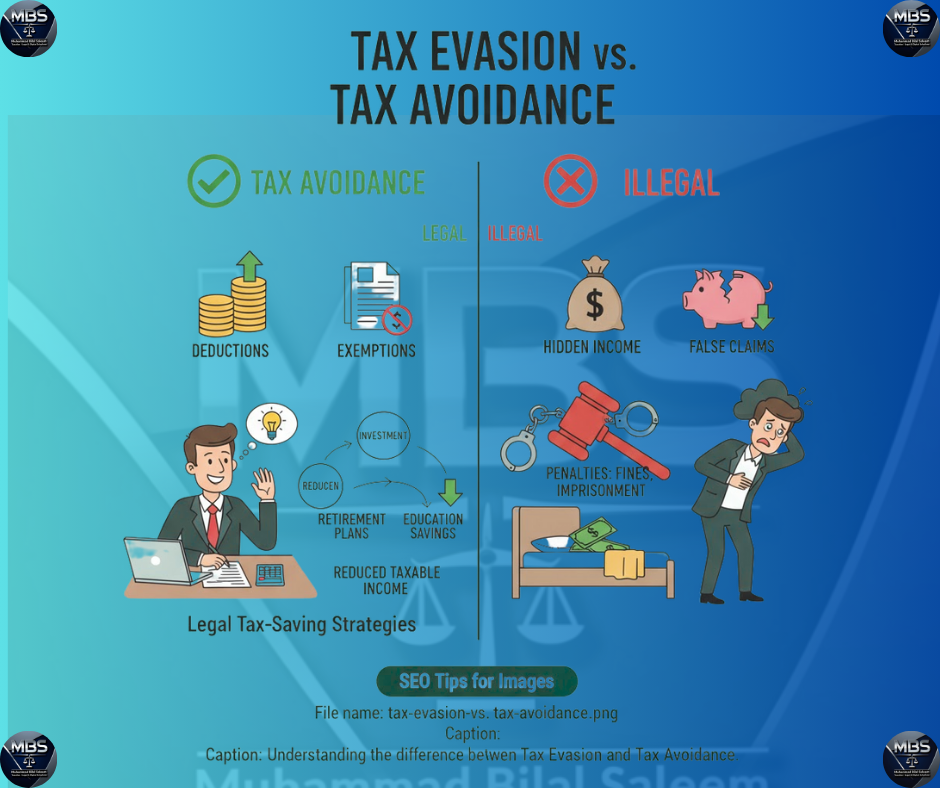

Potential Penalties for Non-Compliance

Non-adherence to the Finance Act 2025 can precipitate severe penalties. It is vital for taxpayers to comprehend the repercussions of non-compliance, encompassing fines and the specter of legal repercussions, to ensure adherence to all statutory obligations.

Tax Saving Opportunities

The Finance Act 2025 also ushers in novel avenues for tax minimization through the introduction of deductions and credits. A thorough understanding of these provisions can empower taxpayers to curtail their tax liabilities effectively.

| Category | Previous Provision | New Provision under Finance Act 2025 |

|---|---|---|

| Tax Filing Deadline | September 30 | October 31 |

| Penalty for Late Filing | 5% of tax due | 7% of tax due |

| Tax Credit for Charitable Donations | Allowed up to 20% of donation | Allowed up to 30% of donation |

Key Highlights of the Finance Act 2025 Tax Changes in Pakistan

The Finance Act 2025 heralds a paradigm shift in Pakistan’s fiscal landscape, with a focus on catalyzing economic expansion. These reforms are poised to exert both immediate and enduring influences on the nation’s economic trajectory.

Major Tax Reforms Overview

The Finance Act 2025 introduces a suite of tax reforms, encompassing novel income tax brackets, recalibrated corporate tax rates, and adjustments to withholding tax mechanisms. These measures are strategically crafted to incentivize investment and stimulate economic advancement.

Key tax reforms include:

- New income tax slabs for salaried individuals

- Revised corporate tax rates to encourage business growth

- Changes in withholding tax to streamline tax collection

Economic Impact Projections

The anticipated economic repercussions of the Finance Act 2025 are projected to be overwhelmingly positive, spanning both the immediate and distant horizons.

Short-term Revenue Implications

In the immediate term, the Act is forecasted to augment government revenue through enhanced tax compliance and elevated tax rates.

Long-term Economic Benefits

Conversely, the long-term implications of these reforms are anticipated to be transformative, fostering a surge in investment, economic expansion, and employment opportunities.

The following table encapsulates the projected economic repercussions of the Finance Act 2025:

| Economic Indicator | Short-term Impact | Long-term Impact |

|---|---|---|

| Government Revenue | Increase | Stable Growth |

| Investment | Moderate | Significant Increase |

| Economic Growth | Stable | Accelerated |

Income Tax Reforms for Individuals

The Finance Act 2025 has ushered in profound alterations to the income tax framework for individuals in Pakistan. These reforms are intended to alleviate the tax load on individuals and stimulate investment in critical sectors.

New Tax Slabs for Salaried Individuals

The tax slabs for salaried individuals have undergone revision, aiming to offer relief to the middle-income bracket. The Finance Act 2025 stipulates the following tax brackets for salaried individuals:

- Up to PKR 600,000: 0% tax

- PKR 600,001 to PKR 1,200,000: 5% tax

- PKR 1,200,001 to PKR 2,400,000: 10% tax

- PKR 2,400,001 to PKR 4,800,000: 15% tax

- Above PKR 4,800,000: 20% tax

Revised Rates for Non-Salaried Taxpayers

Non-salaried taxpayers will witness modifications in their tax rates. The revised rates are designed to streamline the tax structure and diminish the number of tax brackets.

“The simplification of tax rates is a step in the right direction,” opines a tax expert, underscoring the likelihood of enhanced compliance.

Changes in Tax Credits and Deductions

The Finance Act 2025 has introduced alterations in tax credits and deductions to foster investment and expenditure in key sectors.

Education and Health Expense Deductions

Taxpayers are now eligible to claim deductions for education and health expenses. This initiative is anticipated to stimulate spending in these vital sectors.

Investment-Related Tax Credits

Investment-related tax credits have been revised to incentivize investment in specific industries. For example, investments in the manufacturing sector now attract a higher tax credit.

The modifications are expected to enhance economic activity by incentivizing investments.

As articulated by the Finance Minister,

“These reforms are crafted to stimulate economic growth while ensuring a fair and equitable tax system.”

Corporate Taxation Updates

The Finance Act 2025 heralds a transformative era for corporate taxation in Pakistan, ushering in a plethora of revisions. These alterations promise to significantly influence the fiscal landscape, necessitating vigilance among enterprises nationwide. It is imperative for corporations to remain abreast of these developments.

Revised Corporate Tax Rates

The Finance Act 2025 ushers in revised corporate tax rates, a strategic maneuver aimed at bolstering Pakistan’s competitive edge on the global stage. The recalibrated tax framework is anticipated to foster a more conducive environment for investment and expansion. A government official underscored the intent behind these reforms, stating, “Our objective is to catalyze economic growth and entice foreign capital.”

Association of Persons (AOP) Tax Structure

The Act’s revision of the tax framework for Associations of Persons (AOPs) heralds a paradigm shift. The newly introduced AOP tax structure is poised to streamline compliance and diminish the fiscal burden on AOPs, encouraging the proliferation of collaborative ventures. This initiative is viewed as a strategic move to bolster business partnerships.

Small and Medium Enterprise Tax Provisions

Small and Medium Enterprises (SMEs) are the bedrock of Pakistan’s economic fabric, and the Finance Act 2025 addresses their needs with special tax provisions. These provisions are crafted to alleviate the tax compliance burden on SMEs, affording them the impetus to scale their operations.

Special Incentives for Startups

In a concerted effort to stimulate innovation and entrepreneurship, the Act proffers special incentives for startups. These incentives, encompassing tax reliefs and other benefits, are designed to nurture nascent enterprises and facilitate their ascension in a fiercely competitive milieu. A business magnate opined, “Such incentives are indispensable for the sustenance and proliferation of startups in our contemporary business environment.”

The Finance Act 2025 embodies the government’s dedication to cultivating a more hospitable business milieu in Pakistan. Corporations are urged to meticulously scrutinize these updates to capitalize on the opportunities they present and ensure adherence to the revamped regulatory framework.

Withholding Tax Modifications

The Finance Act 2025 introduces profound alterations to withholding tax regulations in Pakistan, with the objective of expanding the tax base and augmenting revenue collection.

WHT on Property Transactions

The Finance Act 2025 introduces adjustments to withholding tax rates on property transactions. These changes are expected to impact both buyers and sellers in the real estate market. The new rates are as follows:

| Property Type | Old WHT Rate | New WHT Rate |

|---|---|---|

| Residential | 2% | 3% |

| Commercial | 3% | 4% |

Banking Transaction Withholding Changes

Withholding tax on banking transactions has also been modified. The new regulations aim to capture more transactions within the tax net. Key changes include an expanded definition of taxable banking transactions and adjustments to the threshold limits.

Digital Payment WHT Framework

The Finance Act 2025 introduces a new withholding tax framework for digital payments, including transactions through mobile banking and fintech platforms. This move is expected to significantly impact the digital economy.

Mobile Banking and Fintech Implications

The new digital payment WHT framework will require fintech companies and mobile banking services to comply with withholding tax regulations. This includes registering with the tax authorities and deducting tax at the prescribed rates.

The changes in withholding tax regulations under the Finance Act 2025 are set to have a far-reaching impact on various sectors, including real estate, banking, and digital payments. It is imperative for taxpayers and businesses to comprehend these modifications to ensure compliance.

Section 7E: Deemed Income Tax on Immovable Properties

The Finance Act 2025 has introduced Section 7E, significantly altering the deemed income tax regime for immovable properties. This legislative amendment seeks to expand the tax base and enhance revenue generation.

Latest Exemptions and Relief Measures

The Finance Act 2025 has introduced novel exemptions and relief measures under Section 7E. These include exemptions for properties dedicated to agricultural purposes and specific residential categories. Taxpayers can benefit from these exemptions by verifying that their properties meet the stipulated criteria.

Valuation Mechanisms and Rates

The Act has revised the valuation mechanisms and rates for determining deemed income tax on immovable properties. The updated rates are contingent upon the property’s location, size, and usage. A detailed table outlining these rates is provided below:

| Property Location | Property Size | Tax Rate |

|---|---|---|

| Urban | Up to 250 sq. yards | 0.5% |

| Urban | Above 250 sq. yards | 1.0% |

| Rural | All sizes | 0.25% |

Compliance Requirements

Taxpayers must adhere to the new regulations by filing their returns and paying the deemed income tax on immovable properties. Non-compliance may incur penalties and fines. It is advisable for taxpayers to seek the counsel of tax professionals to ensure compliance with the necessary requirements.

Key Compliance Deadlines:

- Filing of returns: September 30, 2025

- Payment of tax: October 31, 2025

By comprehending and adhering to Section 7E’s provisions, taxpayers can avert penalties and contribute to the national treasury.

Digital Economy Taxation

The Finance Act 2025 heralds a paradigm shift in the taxation of the digital economy, profoundly impacting entities engaged in e-commerce, digital service provision, and cross-border transactions.

E-Commerce Tax Provisions

Revisions to tax provisions for e-commerce are introduced, mandating platforms to adhere to enhanced reporting and withholding tax obligations. This initiative is designed to bolster tax revenues from the burgeoning e-commerce sector.

Digital Services Tax Framework

A novel framework for taxing digital services is established, targeting entities that offer digital services to Pakistani consumers. This encompasses streaming services, online advertising, and digital marketplaces.

Cross-Border Digital Transactions

The Finance Act 2025 also addresses cross-border digital transactions, ensuring that foreign entities providing digital services to Pakistan are subject to local tax regulations.

International Tax Compliance

Pakistan has harmonized its digital economy tax regulations with global standards to ensure international tax compliance. This alignment reduces the risk of double taxation and guarantees that foreign entities contribute to the local tax base.

| Tax Category | Previous Rate | New Rate (Finance Act 2025) |

|---|---|---|

| E-Commerce Sales Tax | 12% | 15% |

| Digital Services Tax | 8% | 10% |

| Cross-Border Digital Transactions | 5% | 7% |

Sales Tax Reforms

The sales tax environment in Pakistan is undergoing a profound metamorphosis with the implementation of the Finance Act 2025. This legislation introduces a plethora of reforms aimed at optimizing the sales tax system’s efficiency and augmenting revenue collection.

Revised Sales Tax Rates

The Finance Act 2025 revises sales tax rates to align with the government’s fiscal objectives. The newly established rates are crafted to diminish the tax load on specific sectors while concurrently increasing revenue from others.

| Category | Previous Rate | New Rate |

|---|---|---|

| Essential Goods | 5% | 3% |

| Luxury Goods | 15% | 18% |

Zero-Rating Provisions for Key Sectors

The Act introduces zero-rating provisions for critical sectors such as exports and certain industrial inputs. This initiative is anticipated to enhance the competitiveness of export-oriented industries and diminish the production costs for manufacturers.

Input Tax Credit Adjustments

Modifications have been implemented to the input tax credit mechanism to streamline the compliance process for enterprises. These adjustments include more explicit guidelines on what constitutes eligible input tax credits.

Documentation Requirements

To qualify for the input tax credit, businesses must maintain meticulous documentation, encompassing invoices and payment records. This stipulation ensures transparency and facilitates audits.

Customs and Excise Duty Amendments

The Finance Act 2025 has ushered in profound alterations to customs and excise duty frameworks within Pakistan. These revisions are crafted to catalyze economic expansion and enhance trade facilitation.

Import Duty Modifications

The Finance Act 2025 introduces revisions to import duty rates, with the objective of safeguarding local industries while fostering the importation of critical goods. These adjustments are anticipated to positively influence the nation’s trade equilibrium.

Export Facilitation Measures

To augment exports, the Act introduces export facilitation measures, encompassing streamlined customs protocols and diminished documentation requisites. These innovations are poised to enhance the competitiveness of Pakistani commodities on the international stage.

Sector-Specific Customs Provisions

The Finance Act 2025 further incorporates sector-specific customs provisions to bolster critical sectors such as textiles and agriculture. These provisions are engineered to foster economic proliferation and vocational opportunities.

Impact on Manufacturing and Trade

The revisions to customs and excise duty are projected to exert a profound influence on manufacturing and trade within Pakistan. By diminishing the expense of imports and simplifying export processes, the Act endeavors to stimulate economic advancement and augment the competitiveness of Pakistani enterprises.

Conclusion: Navigating the New Tax Landscape in Pakistan

The Finance Act 2025 has ushered in a paradigm shift in Pakistan’s taxation framework, influencing income tax, sales tax, and customs duty. To adeptly navigate this new terrain, taxpayers must grasp the implications of the finance act 2025 and adapt to the evolving regulatory landscape.

Significant alterations include the revision of tax brackets for individuals, the adjustment of corporate tax rates, and the refinement of withholding tax regulations. It is imperative for taxpayers to remain abreast of these reforms to ensure compliance and leverage new avenues for tax savings.

The anticipated outcomes of the act are promising, poised to stimulate investment and catalyze economic growth. As the tax environment continues to transform, taxpayers must vigilantly monitor updates and adjust to the new norms. This proactive stance will contribute significantly to the development of a more resilient and efficient tax system in Pakistan.

FAQ

What is the Finance Act 2025, and why is it significant?

The Finance Act 2025 represents a legislative milestone, aimed at reforming Pakistan’s tax framework. Its primary objectives include revenue enhancement, economic stabilization, and the promotion of growth. This act is a testament to the government’s commitment to fiscal prudence and economic development.

What are the key objectives of the Finance Act 2025?

The Finance Act 2025 seeks to augment revenue streams, streamline tax compliance, and curb tax evasion. It also aims to foster investment and stimulate economic expansion, embodying a holistic approach to fiscal policy.

How does the Finance Act 2025 impact individual taxpayers?

For individual taxpayers, the Finance Act 2025 introduces nuanced income tax brackets for salaried employees and non-salaried taxpayers. It also revises tax credits and deductions, aiming to alleviate the tax burden and incentivize investment.

What are the corporate taxation updates in the Finance Act 2025?

The Finance Act 2025 revises corporate tax rates, introducing tailored provisions for Small and Medium Enterprises (SMEs). It also offers special incentives for startups, designed to nurture innovation and entrepreneurship.

How does the Finance Act 2025 affect the digital economy?

The Finance Act 2025 introduces tax provisions for e-commerce, digital services, and cross-border digital transactions. These measures ensure compliance with international tax standards, expanding the tax base and promoting digital economic growth.

What are the sales tax reforms introduced by the Finance Act 2025?

The Finance Act 2025 revises sales tax rates and introduces zero-rating provisions for critical sectors. It also adjusts input tax credits, simplifying the sales tax compliance process and fostering economic activity.

How does the Finance Act 2025 impact customs and excise duty?

The Finance Act 2025 introduces substantial amendments to customs and excise duty, including modifications to import duty and export facilitation measures. It also provides sector-specific customs provisions, supporting key industries and promoting economic growth.

What are the implications of Section 7E of the Finance Act 2025 regarding deemed income tax on immovable properties?

Section 7E of the Finance Act 2025 addresses deemed income tax on immovable properties, introducing exemptions and relief measures. It also modifies valuation mechanisms and rates, necessitating compliance from taxpayers.

What are the withholding tax modifications introduced by the Finance Act 2025?

The Finance Act 2025 introduces significant changes to withholding tax (WHT) on property transactions, banking transactions, and digital payments. These modifications aim to broaden the tax base and enhance revenue collection.

How can taxpayers ensure compliance with the Finance Act 2025?

Taxpayers must familiarize themselves with the new tax laws, regulations, and requirements of the Finance Act 2025. Seeking professional advice is advisable to avoid penalties and capitalize on new tax saving opportunities.