1. Introduction:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The Finance Act 2025 has introduced one of the most significant tax reforms in Pakistan’s history. Designed to strengthen the country’s revenue base, enhance tax compliance, and improve transparency, these changes affect individual taxpayers, small businesses, corporate entities, and overseas Pakistanis alike.

This article will walk you through all major updates, their practical implications, and tips to stay compliant — so you can avoid unnecessary penalties while optimizing your financial planning.

2. Key Objectives of Finance Act 2025:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The government rolled out these reforms with multiple objectives:

- Boost Revenue Generation – Closing tax gaps by targeting under-reported income.

- Encourage Digital Compliance – Expanding e-filing and electronic payment systems.

- Expand Tax Base – Bringing non-filers and informal sectors into the documented economy.

- Improve Transparency – Automated systems to reduce manual errors and corruption.

- Align with International Standards – Making Pakistani tax laws compliant with global trade and investment requirements.

3. Major Reforms Introduced:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

3.1. Revised Tax Brackets:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The income tax slabs have been restructured:

- Salaried individuals now benefit from lower taxes in income brackets under PKR 1.2 million annually.

- Higher tax rates apply to high-net-worth individuals earning over PKR 10 million yearly.

Example:

If your annual income is PKR 1.5 million, your tax liability will now be 7% lower compared to last year.

3.2. Introduction of E-Invoicing:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

Mandatory electronic invoicing is now in place for:

- Businesses earning above PKR 5 million annually

- Freelancers exporting digital services

- Retailers operating point-of-sale (POS) systems

This ensures real-time reporting of sales and reduces tax evasion.

Tip: Use FBR-approved e-invoicing software to avoid non-compliance notices.

3.3. Withholding Tax Adjustments:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The withholding tax (WHT) regime has been streamlined:

- Lower rates for filers (1% on bank transactions above PKR 50,000 daily).

- Non-filers now face higher deductions, encouraging them to register with the FBR.

3.4. Overseas Pakistanis:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The government has incentivized remittance declarations:

- Tax credits for overseas investors in local startups.

- Exemption on foreign income remitted through official channels.

3.5. Enhanced Penalties:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

Failure to comply with these new provisions can result in:

- Hefty fines starting at PKR 25,000 for non-compliance with e-filing.

- Account freezing for repeated violations.

- Legal action for fraudulent reporting.

4. Impact of Reforms on Different Groups:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

| Category | Impact |

| Salaried Employees | Slight tax relief for mid-level incomes but stricter documentation requirements. |

| Small Businesses | Higher compliance burden due to mandatory e-invoicing. |

| Corporates | Increased reporting standards and audit transparency. |

| Overseas Pakistanis | Better investment incentives but stricter declaration rules. |

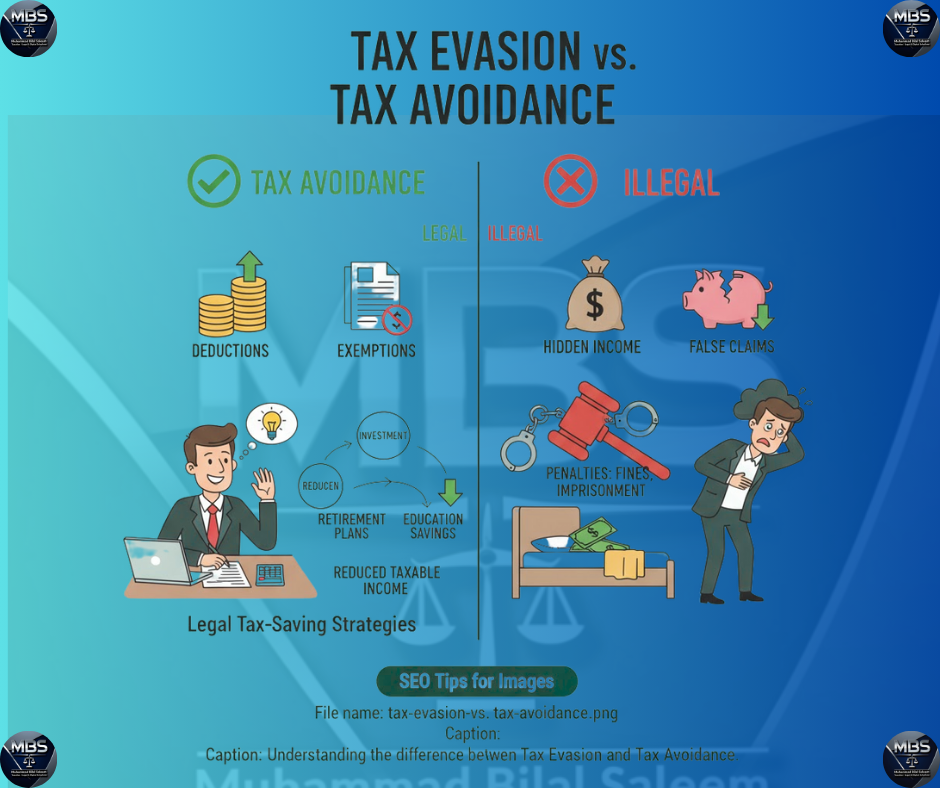

5. Benefits of Compliance:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

- Avoid unnecessary penalties.

- Access to government incentives and rebates.

- Simplified loan approvals from banks and financial institutions.

- Increased business credibility and trustworthiness.

6. Challenges for Taxpayers:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

Despite the benefits, taxpayers may face hurdles such

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Knowas:

- Limited awareness about digital filing systems.

- Lack of training for small businesses.

- Delays in the integration of POS systems with FBR’s servers.

7. Tips to Stay Compliant:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

- Register or update your profile on the FBR portal.

- Use certified e-invoicing software for digital records.

- Keep all receipts and transaction records safe.

- Consult a tax advisor for complex transactions.

- Monitor FBR notifications for ongoing updates.

9. Future Outlook:Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The Finance Act 2025 is just the first phase of a larger reform plan. By 2026, expect:

- AI-driven audits for improved accuracy.

- Enhanced integration between banks, NADRA, and FBR.

- Further digitalization to eliminate paperwork completely.

10. INCOMvE TAX:

The proposal to omit exemptions relating to withdrawal from Approved Pension Funds has been dropped.

1. The proposal to withdraw exemption relating to pension and annuity from former employers has been approved and consequently, such amounts have become taxable with effect from July 1, 2025 under final tax regime at a reduced rate. Commutation of pension will, however, remain exempt from tax.

2. The Commissioner is now empowered to issue full exemption certificates to public limited companies (as compared with existing powers to issue a reduced rate certificate upto 50% of the applicable withholding tax rate).

3.The concept of ineligible persons barring them from undertaking certain economic transactions as proposed through FB has been adopted whereas the bar proposed on ineligible persons to open / maintain bank accounts has been withdrawn. Furthermore, a (new) ‘Fifteenth Schedule’ has been inserted in the Ordinance prescribing thresholds and other conditions relating to its applicability. These provisions shall take effect from the date which the Federal Government specifies by way of an official gazette.

4.The FB earlier proposed to altogether omit the time limitation of 180 days prescribed to pass an amendment assessment order from the date of issuance of a show cause notice. Through FA, the time limit has been enhanced from 180 days to 1 year.

5. The Commissioner has been empowered through FA to allow exemption to a seller from withholding tax on sale of immovable property where such property was held by the seller for at least 15 years, was duly declared in wealth statements filed and was also being used by the seller for his personal use during those years. This exemption is, however, available only once in 15 years. Furthermore, such disposal would be excluded from the applicability of Super Tax under section 4C.

6. A corporate entity being a recipient of a dividend relating to the component of income earned by mutual funds from debt securities shall be taxed at the corporate tax rate of 29%.

7.Rate of withholding income tax on payments for digital transactions in E-commerce platforms is now prescribed at 1% for digital means or banking channels and 2% for Cash on Delivery Transactions. Page 2 of 4

8. All of the Non-Profit Organisations (NPOs) mentioned in Table 1 of Clause (66) were proposed through FB to be subjected to conditions of section 100C. Through FA, unconditional exemption for certain NPOs has been restored by placing them under Clause (57).

9.The concept of minimum fair market rent for commercial properties proposed through FB to be introduced has been withdrawn.

10.The FB proposed to disallow 10% of the claimed expenditure attributable to purchases from persons who are not National Tax Number holders, except for agricultural products directly purchased from growers. Amendment through FA in the said clause now provides that such disallowance will be made only in case of purchase of agricultural produce from the middleman.

11. Provisions introduced through Tax Laws (Amendments) Ordinance 2025 for immediate recovery on issues decided in favour of the Tax Department have been rationalised. Now, such recovery may be made only when the issue has been decided by at least 3 appellate forums (including the High Court) and the amount of tax also exceeds Rs. 200 million. It has further been provided that the amount of tax recovery shall be the lowest amount of demand confirmed by any of the 3 appellate forums. However, the proposal through FB to issue at least 7 days’ prior notice has been withdrawn.

12. The higher rate of CGT of 20% prescribed through FB for non-resident investors investing in debt instruments and Government securities through Special Convertible Rupee Accounts was proposed to be applicable for holding periods of less than 12 months. As per FA, such a higher rate will apply for a holding period of less than 6 months.

13. The FB proposed to enhance the rate of tax deduction from 15% to 20% on yield or profit received by a person from a banking company or financial institution on an account or deposit maintained with such company or institution. Through FA, the increased rate of 20% has now been also made applicable to profit or yield received by a person (other than individuals) from government securities (other than National Savings etc.) which will also be final tax for AOPs earning profit-on-debt upto Rs. 5 million.

14. Tax withholding rates applicable on purchase of immovable property by persons not appearing in the Active Taxpayers List have been reduced with

whereas the rates applicable on sale of immovable property by such persons has been enhanced.

15. A penalty proposed in FB for an online marketplace allowing an unregistered vendor (required to obtain sales tax as well as income tax registration) to operate on its platform has been withdrawn.

11.SALES TAX :

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

. The Abettor now means a person who intentionally abets or connives in tax fraud. Further, certain specific instances earlier covered therein, relating to misusing the login credentials and obtaining sales tax registration for paper transactions, have been excluded.

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

1. Food delivery platforms and e-commerce delivery service providers, earlier proposed to be included in definition of ‘courier’, are now excluded from the purview thereof meaning thereby that they are not liable to collect and pay sales tax in case of supply of digitally ordered taxable goods. Page 3 of 4

2. FB proposed sales tax withholding by payment intermediary and courier at the rate of 2% of value of supplies, which was proposed to be deemed as final tax, without any adjustment of input tax. It has now been provided that such final taxation would apply only on cottage industry and retailers (other than tier-I retailers). As a result, such persons are not required to be registered for sales tax purposes for selling their goods through e-commerce platforms, provided that they hold NTN.

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

3. Before permanently barring a person’s bank account due to non-registration, the Commissioner is now required to firstly suspend the account operations intermittently 3 times. Each suspension would last for 3 working days, with a one-week interval between each suspension. This action may be taken only if the Commissioner believes the person is supplying taxable goods without registration under the Sales Tax Act and has ignored 3 opportunities to register.

4. The FA provides that if a person does not obtain registration within 15 days after suspension of bank accounts, the Chief Commissioner shall form a committee to address the issue. This committee will issue a notice to the person and offer a personal hearing. The committee will then recommend whether to impose a restriction on transferring immovable property or to lift the restriction on bank account operations. However, the person will be given an additional 15 days to secure registration before the recommendation to impose the restriction is made.

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

5. Penalties, presently specified under the Sales Tax Act in respect of non-integration by Tier-1 retailers, have been extended to all registered persons which are required to be integrated but fail to do so.

6. Penalties / prosecution earlier proposed for committing tax fraud, abetting or conniving to commit tax fraud and failure on part of online marketplace to file monthly statements have been reduced / rationalised.

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

7. Power to arrest a person accused of tax fraud or subject to prosecution have been further rationalised. Now, such a person may be arrested, after investigation, only if it is established that: the accused is intentionally or willfully not joining the investigation after 3 duly served notices; the accused is attempting to abscond; or there are sufficient grounds that the accused would temper with the evidence.

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

8. The proposal to grant the investigation officer the powers available to a Police officer in-charge of a police station under the Code of Criminal Procedure, 1898 has been withdrawn.

9. Explicit powers to arrest CEO and CFO of companies involved in tax frauds have been withdrawn.

12. Conclusion:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

The Finance Act 2025 marks a major step towards a more transparent and modern tax ecosystem in Pakistan. While the changes bring challenges in terms of digital adaptation, they also open doors for greater efficiency, reduced fraud, and improved revenue collection.

To stay ahead, taxpayers should embrace digital solutions, seek expert advice, and remain updated on the evolving legal landscape.

FAQ:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

Q1: Who must comply with these 2025 amendments?

All registered taxpayers, including salaried individuals, business owners, property owners, investors, and non-resident Pakistanis.

Contact Us:

Expanding Tax Reforms from Finance Act 2025: What Every Taxpayer Needs to Know

Follow us on social media for updates, tips, and tax humor:

- Facebook: MBS Taxation

- Website: MBS Taxation

- Our Website Contact Form: Click Here

- Whatsapp Number: +923087543324

We’re here to simplify your taxes so you can focus on what matters most—your work, business, and life!